The Covenant Homeownership Act mandates that the eligibility requirements must include:

To check if you're eligible, complete the form below:

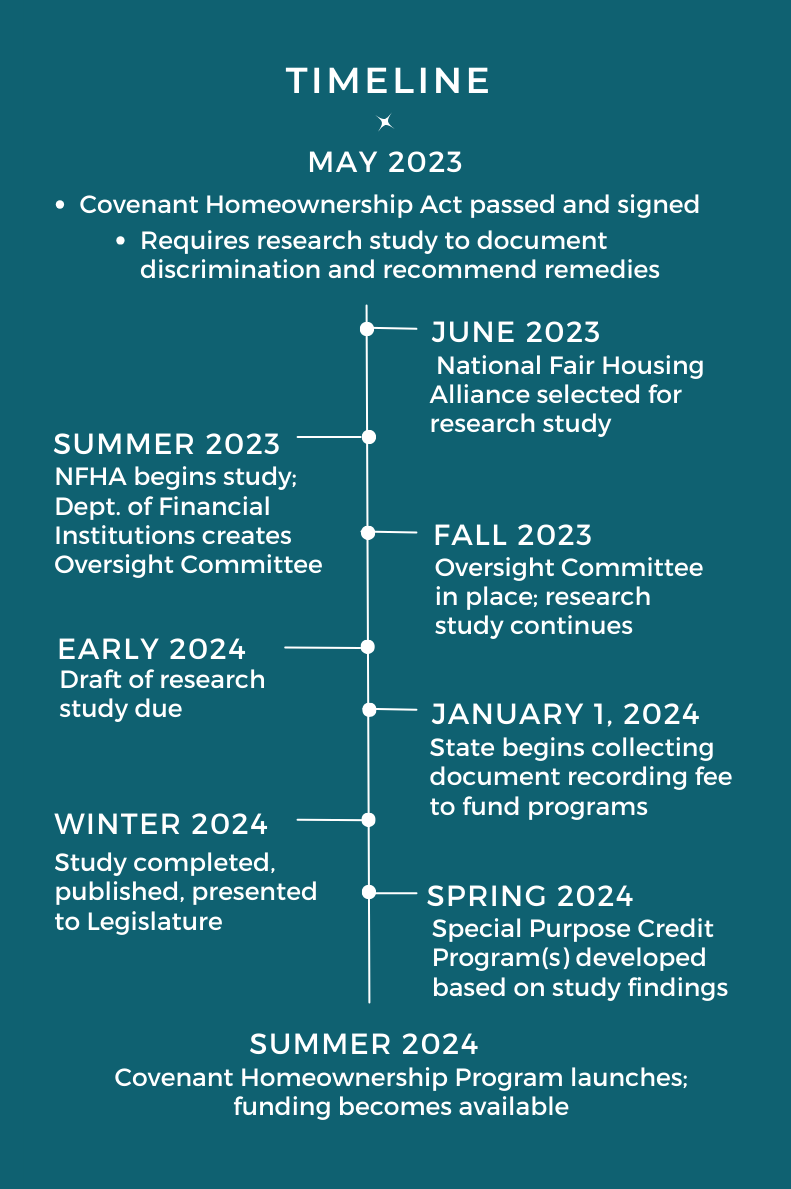

In spring 2023, thanks to the advocacy and leadership of the Housing Development Consortium, the Black Home Initiative, Rep. Jamila Taylor, Sen. John Lovick, and Rep. Frank Chopp, the Washington State Legislature passed the Covenant Homeownership Act with bipartisan support. This landmark legislation makes us the first state to face and address the role of government institutions in housing-related discrimination and racism.

March 2024: Covenant Homeownership Study Released

This study is required by the Covenant Homeownership Act in order to establish the framework for the Covenant Homeownership Program. It examines the history of housing discrimination in Washington state, what role government institutions have played, the ongoing impacts of discrimination, and what programs can remedy these impacts.

The Covenant Homeownership Act

The term “covenant” refers to the racially restrictive clauses used in neighborhoods throughout the state of Washington in order to keep people out based on their race or religion. The Covenant Homeownership Act represents a new commitment to correct this injustice (and others such as redlining) and help families begin building wealth through homeownership.

The new law has two important parts:

1. A research study to investigate housing discrimination against marginalized communities in Washington State, what role government institutions have had in the discrimination, the impacts of the discrimination, and potential remedies for the impacts. These findings will help determine who will be eligible for assistance and establish the framework for creation of a Special Purpose Credit Program under the Equal Credit Opportunity Act.

2. A new source of funding for homebuyer assistance from a new $100 document recording assessment on every real-estate transaction. These fees will be deposited into the Covenant Homeownership Account and fund the Special Purpose Credit Program, which will be designed and implemented based on the findings of the research study.

What is the Covenant Homeownership Study?

The study is the first, crucial step in the development of Covenant Homeownership Act assistance programs. This evidence-based research study investigates housing discrimination against marginalized communities in Washington State, what role government institutions have had in the discrimination, the impacts of the discrimination, and what specific assistance would be likely to remedy these impacts.

Who conducted the Covenant Homeownership Study?

As the result of a competitive process, National Fair Housing Alliance (NFHA) was selected to conduct the study, overseen by the Washington State Housing Finance Commission (Commission).

The National Fair Housing Alliance, the lead consultant, has a 33-year history of documenting historical and current discrimination to identify, eliminate and remedy the harms that have resulted. They also bring significant expertise with special-purpose credit programs.

Abt Associates, the key research partner in the study, is a mission-driven research and consulting firm with deep expertise in publicly administered homeownership programs, data analysis, and fair housing.

NFHA and Abt will also be joined by two Washington state groups with years of knowledge and expertise in fighting housing discrimination in our state. The Northwest Fair Housing Alliance (NWFHA), serving central and eastern Washington, and the Fair Housing Center of Washington (FHCW), based in western Washington, will subcontract with NFHA to assist in documenting specific historical discrimination against marginalized groups in Washington.

How was this contractor selected?

National Fair Housing Alliance and its research partners were chosen through a competitive Request for Proposals process in 2023.

How were community members and stakeholders involved in the study?

NFHA and its local fair housing partners incorporated numerous points of active community engagement with stakeholders, from webinars and presentations to key informant interviews, focus groups, and surveys. Many Washington residents shared their personal and family experiences with housing discrimination. Summaries of these stories can be found in Chapters 1 and 2 of the study and in the appendices for these chapters.

What are the key findings of the study?

First of all, the study confirms that state institutions played both active and passive roles in perpetuating housing discrimination against a range of marginalized groups. Secondly, it finds that impacts of that discrimination are still felt today in the lower homeownership rates and net worth of many of those groups. Third, the research shows that without specifically aiming to help these groups that were excluded for so long, a program would be ineffective in remedying the disparities.

What are the study’s recommendations?

The study recommends a Special Purpose Credit Program with a customized approach to downpayment assistance that allows people who have been impacted by discrimination to buy a home in their county.

Such a program has the flexibility to support homeownership in a way that a normal downpayment assistance program would not, in two ways. First, it could offer a large enough loan to make a home attainable in the county where they live for anyone who qualifies; and second, it would be exclusively available to groups who both suffered housing discrimination by state institutions in the past and continue to show the effects in disparities today. (The Covenant Homeownership Act includes additional specific eligibility requirements for individuals.)

The study recommends that certain marginalized groups be considered eligible for the program. How did the study come to these conclusions?

The researchers based their recommendations on evidence of two factors: not only racial discrimination by the state in the past, but also disparities in homeownership rates today. The study examined available data for each of the marginalized groups affected by past housing discrimination. While many groups of Washingtonians, such as those named in racist homeowner covenants, have suffered significant harms from housing discrimination, not all these groups continue to show significantly lower homeownership rates than white residents. Those that do are recommended for program eligibility. Homebuyers in any of these recommended groups must also meet individual eligibility requirements (under the income limit, a resident of Washington before 1968 or descendant of such a resident, first-time homebuyer, etc.).

How will the Covenant Homeownership Program help homebuyers?

The Covenant Homeownership Program will provide downpayment and closing cost assistance for first-time homebuyers excluded from homeownership by racially restrictive covenants. These costs are often a significant barrier to homeownership.

When will the Covenant Homeownership Program begin?

The Covenant Homeownership Program will begin serving homebuyers in July 2024.

Who will be eligible for assistance?

The Covenant Homeownership Program Study will use evidence-based research to identify the economically disadvantaged class or classes of persons that require down payment and closing cost assistance to reduce racial disparities in homeownership in Washington. This in turn will shape the eligibility guidelines.

The Covenant Homeownership Act mandates that the eligibility requirements must include:

What will be required of homebuyers using the Covenant program?

All homebuyers must meet lender underwriting requirements, i.e. prequalify for a loan from a lending institution. You must also take a free homebuyer education class, either virtually or in person. Dozens of classes are taught each week by lenders and real-estate professionals across the state.

If you are not quite ready for a mortgage, you can still start your journey to homeownership with free, individual help from a housing counselor, available through a wide network of nonprofit partners. Get connected through the Washington State Homeownership Hotline by calling 1-877-894-4663 or visiting www.homeownership-wa.org.

How will eligible homebuyers access the Covenant Homeownership Program?

Through one of the hundreds of lenders statewide who use the home-loan programs of the Housing Finance Commission. These loan officers are trained in the Commission’s programs and can reserve our home loans and downpayment assistance.

What can I do now if I’m ready to buy a home?

If you’re ready to start your journey toward homeownership now, we encourage you to call the Washington Homeownership Resource Center (WHRC) at 1-877-894-4663 or visit their website at www.homeownership-wa.org.

The Housing Finance Commission also offers home-loan and downpayment assistance programs. You can also find a free homebuyer education class here to get started on your homebuying journey.

Where will the Covenant Homeownership Program funding come from?

Starting in January 2024, the state will collect a $100 document recording assessment for real-estate transactions. The fee is projected to generate between $75 million and $100 million each year and will be deposited into the Covenant Homeownership Account. The account will be used for the purposes of the Covenant Homeownership Program.

Who is responsible for the Covenant Homeownership Program?

The Washington State Housing Finance Commission will design, develop, implement, and evaluate the Covenant Homeownership Program. The Commission is also responsible for overseeing the Covenant Homeownership Program Study that will determine the details of the program.

Who will hold the Commission accountable?

A Covenant Homeownership Program Oversight Committee, formed by the Department of Financial Institutions (DFI), will oversee and review the Commission’s activities and performance related to the Covenant Homeownership Program Study and the Covenant Homeownership Program. The oversight committee may also, from time to time, make recommendations to the legislature regarding the program. DFI will convene the initial meeting of the committee and select a chair by October 1, 2023.

How will you evaluate the effectiveness of the Covenant Homeownership Program?

The Housing Finance Commission will submit an annual report to the legislature on the progress of the Covenant Homeownership Program by December 31, 2025, and by each following December 31. The Commission will complete an update to the Covenant Homeownership Program Study at least every five years to evaluate the program’s effectiveness and recommend Covenant Homeownership Program improvements.

What is a racially restrictive covenant?

Covenants are clauses that prevent, prohibit, restrict, or limit the actions of a person or entity named in a contract. As part of home deeds and required neighborhood agreements (like HOAs), covenants were commonly used between the 1920’s and 1960’s to restrict housing based on race, religion, and ethnicity. A typical covenant required the signer to agree they would never allow a non-white or non-Christian person to buy or live in their home.

Black people were excluded in every racially restrictive covenant. Asian American Pacific Islanders, Latino/a/x, Jewish people, and other marginalized groups were also excluded. To date, nearly 50,000 racially restrictive covenants have been documented throughout Washington state by the Racial Restrictive Covenants Project of the University of Washington and Eastern Washington University.

How are the terms Covenant Homeownership Act, Covenant Homeownership Program, Covenant Homeownership Program Study, and Covenant Homeownership Account related?

The Covenant Homeownership Act is a state law passed in the spring of 2023 to support homeownership for those affected by generations of systematic discriminatory housing policies and practices by Washington State. The act establishes an assistance program (Covenant Homeownership Program) based on an evidence-based study (Covenant Homeownership Program Study). A newly created account in the state treasury (Covenant Homeownership Account), funded by document recording assessments, will be used for the purposes of the program and study.

How did the Covenant Homeownership Act come to pass?

The Covenant Homeownership Act is unique because it began with an extensive stakeholder and community engagement process. In September 2022 the Housing Development Consortium of Seattle-King County (HDC) convened more than 50 stakeholders across multiple sectors who worked together to examine barriers to homeownership as well as policy options that could address these barriers. These comprehensive conversations with possible bill sponsors and champions resulted in a set of suggestions for the legislation.

In addition to shaping the legislation, the stakeholder and community engagement process ensured strong and effective advocacy that led to the bill’s passage with bipartisan support.

Why is the Covenant Homeownership Act needed?

Homeownership is the cornerstone of the American dream. It is the primary way households build wealth, stability, and community and pass wealth down to future generations.

Yet in Washington, only 49% of BIPOC households in Washington are homeowners, compared with 68% of non-Hispanic white households. As is common where disparities exist, Black households fare even worse than other households of color: the homeownership rate for Black households is only 31%. Despite the Fair Housing Act and the end of “legal” discrimination, the national homeownership rate for Black households has not improved since 1960.

Research shows that these inequities did not arise by chance or because of individual choices. They are the result of policies and practices that favored white Washingtonians. Previous research has also shown that existing state and federal programs and other race-neutral approaches are insufficient to remedy this discrimination and its impacts. That is why the Covenant Homeownership Act proposes the first-in-the-nation use of a Special Purpose Credit Program by a government agency.

What is a Special Purpose Credit Program?

Special Purpose Credit Programs were made available by the Equal Credit Opportunity Act of 1974 to benefit a specific class of persons who share common characteristics (for example, race, national origin, or sex). They are an important tool in expanding fair access to credit, particularly for consumers and communities impacted by discrimination.

Why create a Special Purpose Credit Program?

The racial homeownership gap will persist without specific intervention that goes beyond “colorblind” or “race-neutral” assistance. A Special Purpose Credit Program can be race-conscious, allowing our state to directly remedy the harm caused by its discriminatory policies and practices.

Until now, only private businesses have utilized Special Purpose Credit Programs to remedy harm caused by their actions. The Covenant Homeownership Act is the first programmatic use by a government agency to remove persistent structural barriers to homeownership.

Why require a Covenant Homeownership Program Study?

The Covenant Homeownership Program Study provides the foundation for a Special Purpose Credit Program that can benefit homebuyers affected by racial discrimination.

Why does the Covenant Homeownership Act enact a $100 document recording fee?

For many years, Washington state mandated that county auditors record racially restrictive real-estate covenants. Legislators found it fitting that this same document-recording process should help remedy the harm created by these actions.

Is the Covenant Homeownership Act reparations?

The Covenant Homeownership Act begins the process of remedying past and ongoing discrimination and its impacts on access to credit and homeownership for BIPOC and other historically marginalized communities in Washington state. It does not represent a formal reparations effort.

Are you ready to start your journey toward homeownership now? As we work diligently toward the key deliverables of the Covenant Act, here are several resources available for homebuyers:

Free personal financial counseling and preparation for homeownership: Call the Washington Homeownership Resource Center (WHRC) at 1-877-894-4663.

Free homebuyer classes: Free online and in-person classes sponsored by the Housing Finance Commission are offered by home-loan professionals across the state. Find one here.

Downpayment assistance and finding a lender: Visit the Housing Finance Commission’s homebuyer page to find a lender and learn about home loans and downpayment assistance for homebuyers.

{kind=link}